When you pick up a prescription at the pharmacy, you might not think about why one drug costs $10 and another costs $75. But behind that price difference is a complex system designed by your employer’s health plan - one that pushes you toward generic drugs not because they’re less effective, but because they’re far cheaper. And if you don’t understand how this system works, you could be paying way more than you need to.

Why Your Employer Pushes Generic Drugs

Generic medications aren’t just cheaper - they’re the same. The FDA confirms that generic drugs must contain the same active ingredients, strength, dosage form, and route of administration as their brand-name equivalents. They’re held to the same safety and effectiveness standards. The only real difference? Price. Generics cost 80-85% less because manufacturers don’t have to repeat expensive clinical trials or run nationwide ad campaigns. That’s why, every week, generic drugs save the U.S. healthcare system over $3 billion - more than $150 billion a year. Employers didn’t invent this trend. But they’ve embraced it hard. Over 99% of large employer health plans include prescription drug coverage, and nearly all of them structure it around a tiered formulary. This system rewards you for choosing generics. If you pick a brand-name drug when a generic is available, you pay more. Plain and simple.How Tiered Formularies Work

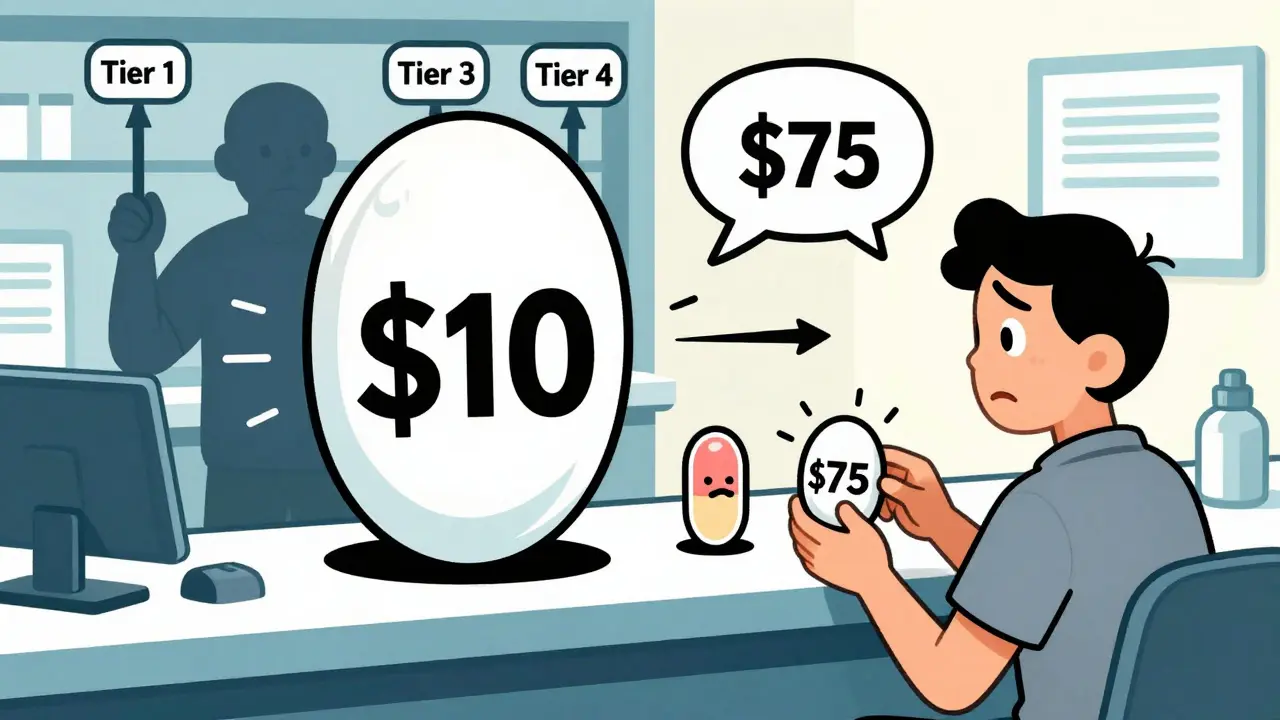

Most employer plans divide drugs into four tiers:- Tier 1: Generics - Lowest cost. Typically $10 copay.

- Tier 2: Preferred Brand-Name - Brand drugs the plan encourages. Usually $40 copay.

- Tier 3: Non-Preferred Brand-Name - Brand drugs the plan discourages. Often $75 or more.

- Tier 4: Specialty Drugs - High-cost medications for complex conditions like cancer or MS. Can cost hundreds or even thousands per month.

Who Controls Your Drug Access? The PBMs

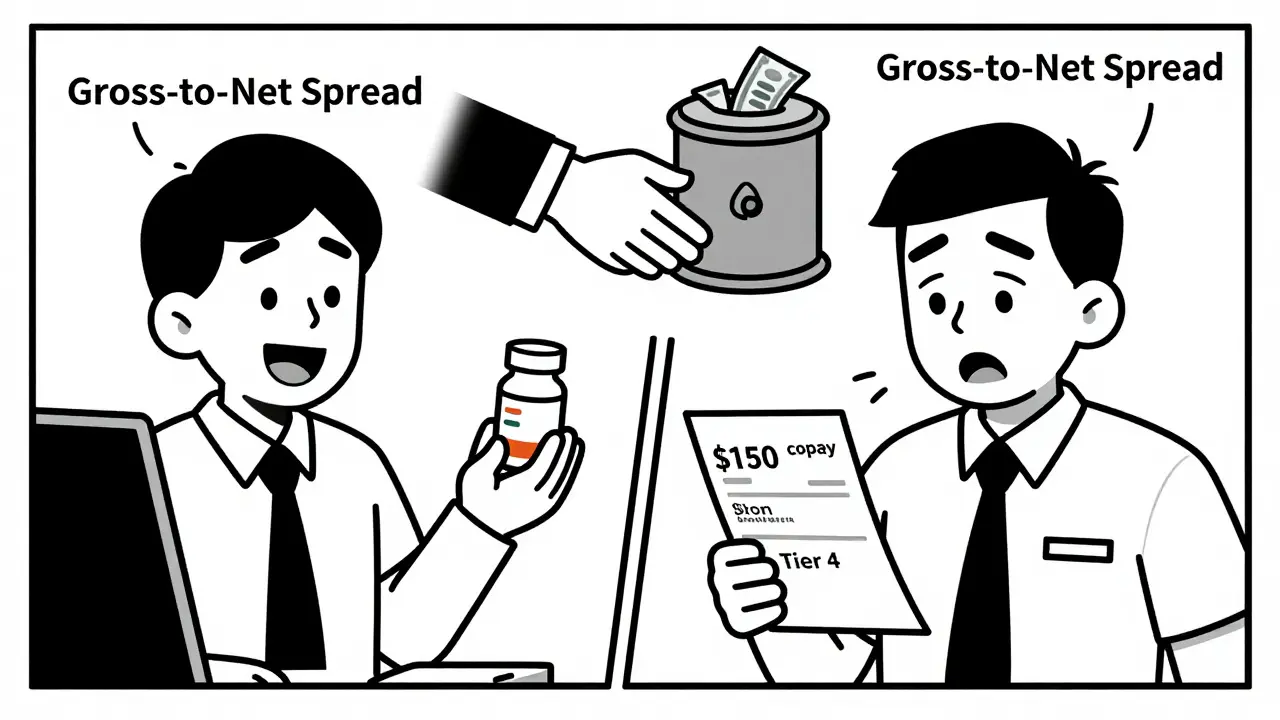

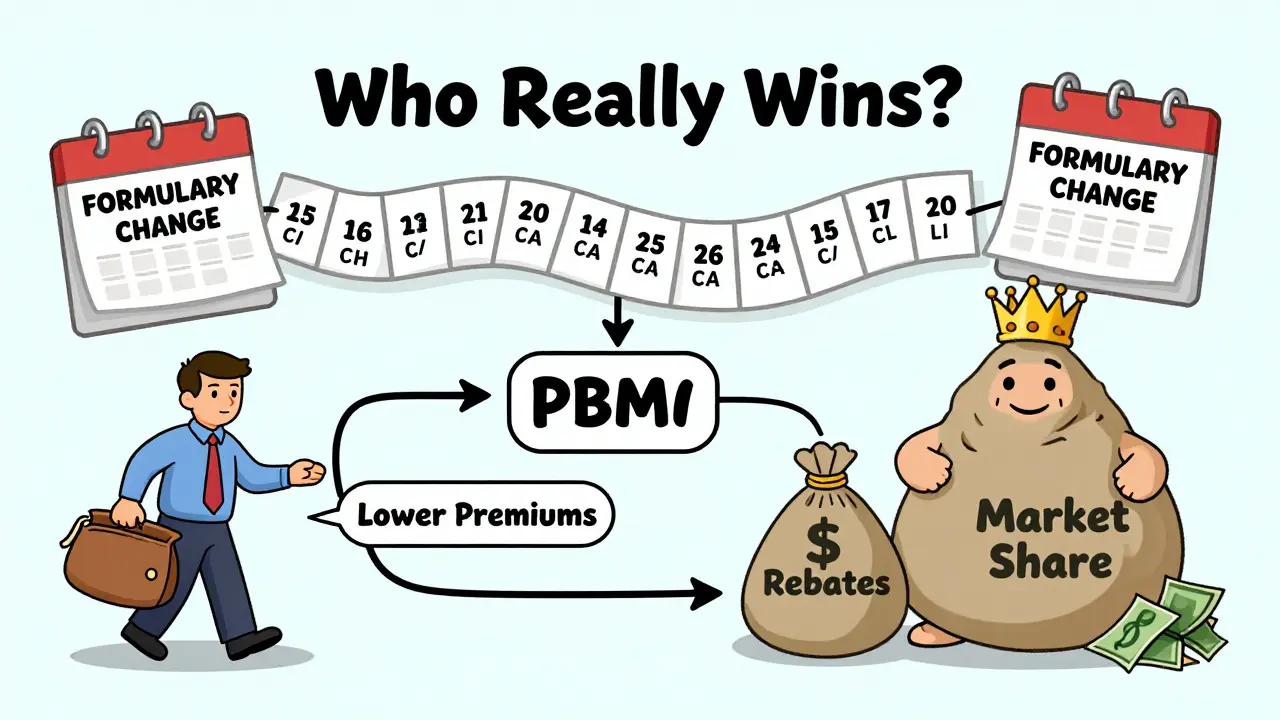

You might think your insurance company decides what drugs are covered. But the real power lies with Pharmacy Benefit Managers (PBMs): OptumRx, CVS Caremark, and Express Scripts. These three companies manage prescriptions for the majority of Americans with employer-sponsored coverage. PBMs don’t just list drugs. They decide which ones get excluded. In January 2024, each of these three PBMs removed more than 600 drugs from their formularies. That’s over 1,800 medications pulled in one month alone. Why? To force drugmakers to offer bigger discounts. If a company doesn’t pay up, its drug gets dropped - and your access to it vanishes. But here’s the catch: the savings from these negotiations don’t always reach you. PBMs use a pricing trick called gross-to-net (GTN) pricing. A drug might have a list price of $100, but after rebates and discounts, the PBM pays only $45. That 55% difference - the GTN spread - goes to the PBM, not you. So even though your employer saved money, your out-of-pocket cost didn’t drop. In fact, you might not even know the drug you’re taking was discounted.

What Happens When Your Drug Gets Removed

If your medication suddenly disappears from the formulary, you’re not out of luck - but you have to act. You might be able to:- Switch to the generic version (if one exists).

- Ask your doctor for a therapeutic alternative - another drug in the same class that’s still covered.

- File a medical necessity exception with your insurer. This requires documentation from your doctor proving you can’t safely switch.

How to Find Out What’s Covered

You can’t rely on memory or past experience. Formularies change constantly. Here’s how to stay in control:- Log in to your insurer’s website and search their drug list. Look for the formulary or drug list section.

- Review your Summary of Benefits and Coverage (SBC). It’s required by law and should include a summary of drug coverage.

- Call your insurer directly. Ask: “Is [drug name] covered? What tier is it on? Is there a generic?”

- Check with your pharmacy. Pharmacists often know about recent formulary changes before you do.

Why You Still Pay More - Even When Generics Save Money

The system is designed to save money - but not always for you. Employers benefit from lower premiums and insurance costs. PBMs profit from rebates. Drugmakers gain market share by paying those rebates. But employees? You’re often left paying the difference. For example: If your employer switches to a plan with a narrow formulary, you might save $200 a month on premiums. But if your diabetes medication got moved to Tier 4, your monthly copay could jump from $20 to $150. You’re worse off. This is why education matters. Many employees are willing to use generics - they just don’t know they’re safe. Or they’ve heard myths about generics being “weaker.” That’s not true. The FDA says they’re identical. Your employer should be telling you this - through emails, payroll inserts, or even text messages. If they’re not, ask them to.What You Can Do Right Now

Don’t wait for your employer to fix the system. Take control:- Always ask your pharmacist: “Is there a generic version?”

- Use in-network pharmacies. Out-of-network fills often aren’t covered at all.

- Ask your doctor to prescribe generics first - even if you’ve always taken the brand.

- Check your formulary every 90 days. Changes happen fast.

- If you’re on a chronic condition like asthma, diabetes, or high blood pressure, ask if your plan has a Chronic Illness Support Program. These often offer extra savings and care management.

What’s Coming Next

The trend is clear: more exclusions, tighter tiers, and more pressure to use generics. PBMs are getting smarter - and more aggressive. Some states are starting to regulate GTN pricing, but federal rules are still weak. Employers will keep pushing generics because it works. The real question is whether they’ll start sharing those savings with you. For now, the best defense is knowledge. Know your plan. Know your drugs. Ask questions. And don’t assume your medication will still be covered next year - because chances are, it won’t be.Are generic drugs really as good as brand-name drugs?

Yes. The FDA requires generic drugs to have the same active ingredients, dosage, strength, and effectiveness as brand-name versions. They’re tested to ensure they work the same way in your body. The only differences are inactive ingredients (like fillers) and cost. Generics are not inferior - they’re just cheaper.

Why does my copay go up even when a generic is available?

Because your plan’s formulary moves the brand-name version to a higher tier - often Tier 3 or 4 - while the generic lands in Tier 1. If you stick with the brand, you pay more. It’s not a glitch; it’s intentional design to steer you toward the cheaper option. You’re not being punished - you’re being incentivized.

Can my employer change my drug coverage without telling me?

Yes. Formulary changes can happen anytime, often with no advance notice. PBMs negotiate deals with drugmakers constantly, and those deals can trigger exclusions or tier shifts overnight. That’s why checking your formulary every few months isn’t optional - it’s essential.

Why don’t I see the savings from generic drugs in my paycheck?

Because the savings often go to your employer’s insurer or the Pharmacy Benefit Manager (PBM), not to you. PBMs negotiate rebates from drugmakers, but those rebates don’t always lower your copay. Instead, they reduce the overall cost of the plan - which might lower premiums, but doesn’t guarantee lower out-of-pocket costs for you.

What if my medication gets removed from the formulary?

You can file a medical necessity exception with your insurer. Your doctor must submit documentation explaining why you can’t switch to another drug. If approved, you’ll still get coverage - but this process takes time. Don’t wait until your refill runs out. Start the process as soon as you hear the drug was removed.

Understanding your employer’s health plan isn’t about becoming a pharmacy expert. It’s about protecting your health and your wallet. The system is built to save money - but only if you know how to play it.

9 Comments

Let me get this straight - you’re telling me I’m supposed to trust a pill that looks nothing like the one I’ve been taking for 12 years? 😅

Generics? Sure. But I’ve seen the packaging. The color’s off. The shape’s weird. The damn thing doesn’t even have the same logo.

And now you want me to believe it’s chemically identical? Bro. I don’t care what the FDA says. My body remembers the brand. It knows the difference. And no, I’m not switching just because my copay went up $65.

Also - who the hell decided I’m supposed to be a pharmacy detective? I pay taxes. I pay premiums. I shouldn’t need a spreadsheet to figure out if my blood pressure med is still covered.

And don’t get me started on PBMs. They’re the middlemen who profit off my confusion. I’m not a line item. I’m a human with a chronic condition.

Yeah, generics save money. But they don’t save dignity. And sometimes, dignity costs more.

Y’all are overcomplicating this. If the generic works, use it. Simple. No drama.

My dad was on brand-name statins for 8 years. Switched to generic - same labs, same energy, half the cost. He’s alive and happy. Case closed.

Stop making this about trust and start making it about results. Your body doesn’t care about logos.

Love this breakdown 🙌

Seriously, I had no idea PBMs were pulling 600+ drugs in a single month. That’s wild.

Just switched to a generic for my anxiety med last month - saved me $80/month. My pharmacist even gave me a sticker 🎉

Turns out, the generic is literally the same pill, just in a plain white capsule. I didn’t even notice the difference.

Also - check out your insurer’s app. Mine has a ‘Drug Swap’ feature that auto-suggests cheaper alternatives. Life changer.

Thanks for the nudge to check my formulary. I’m on it now 😊

There’s a quiet revolution happening here - and most people don’t even realize it.

Generics aren’t just cheaper - they’re democratizing healthcare. For decades, people skipped meds because they cost too much. Now? A $10 copay means someone with diabetes can afford insulin. A $40 tier means someone with high cholesterol can stick with treatment.

Yes, PBMs are shady. Yes, formulary changes are sneaky. But the system isn’t broken - it’s just skewed toward profit, not people.

The real win? When employers start sharing savings with employees instead of just lowering premiums.

Imagine a world where your $200/month premium drop also means your $150 copay drops to $50. That’s not fantasy - that’s policy. We just need to demand it.

Knowledge is power. Keep asking. Keep checking. Keep pushing.

Just wanted to say - I read this after my doctor switched me to a generic for my thyroid med. I was nervous. I thought, ‘What if it doesn’t work?’

Turns out, it worked better. My TSH levels stabilized faster. No side effects. No weird headaches.

I didn’t know generics were held to the same standards. I thought they were ‘second choice’ meds.

Turns out, I was wrong. Thanks for the clarity. I’m going to tell my mom. She’s been on brand-name blood pressure meds for 15 years. She’s gonna be shocked.

My PBM dropped my asthma inhaler last month. No warning. No email. Just ‘out of stock’ at the pharmacy.

Had to call 3 doctors, file an exception, and wait 11 days to get it back.

Meanwhile, I was using my rescue inhaler every other day. That’s not ‘incentivizing’ - that’s negligence.

Also - why do PBMs get to be the gatekeepers? They’re not doctors. They’re not insurers. They’re corporate middlemen with Excel sheets and no conscience.

😤

Don’t wait for your employer to help you. Be proactive.

Check your formulary. Ask your pharmacist. Call your insurer.

It takes 5 minutes. And it could save you $1000 a year.

You’re worth it. 💪

There’s a hidden layer here most people miss - the role of pharmacists.

They’re the frontline. They see every formulary change before you do. They know which generics are reliable, which are sketchy, and which ones your body might react to differently.

I used to think pharmacists just handed out pills. Now I know - they’re your best ally.

Build a relationship with yours. Ask questions. Say ‘I’m on a tight budget - is there another option?’

They’ll help. They want you to be healthy.

And if they don’t? Find a new pharmacy. Your health isn’t a transaction.

Think about this: the entire system is built on a lie.

We were told generics are ‘equivalent.’ But the truth? They’re not always *identical* - just *therapeutically equivalent*. There’s a difference.

Some people metabolize drugs differently. A 5% variation in inactive ingredients? For some, it’s the difference between relief and disaster.

And yet - we’re punished for wanting the brand.

It’s not about cost anymore. It’s about autonomy.

When did we decide that corporate efficiency should override individual physiology?

I’m not against generics. I’m against coercion.

What if the system didn’t punish you for being vulnerable - but protected you for being human?

That’s the future we need to fight for. Not just cheaper pills. Fairer care.